Many of our efforts as Blacktivists focus on helping Black Canadians improve their economic situation. However, if Black folks aren’t financially literate, any money they get will go in one hand and out the other – and the hand it goes out to likely won’t be Black. Financial literacy is crucial to building inter-generational wealth. But what does it mean to be financially literate?

Well, in addition to basics like budgeting, financially literacy means knowing how to:

- Break the cycle of falling prey to predatory lenders

- Find out, and improve your credit score; and

- Reduce your taxes.

Avoid payday loans

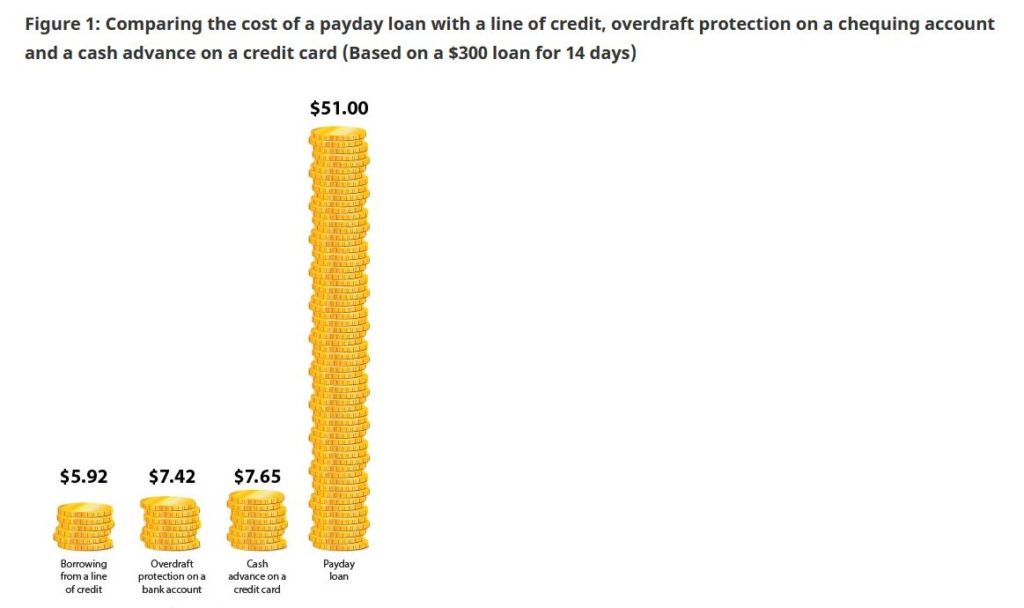

Predatory lenders like payday loan companies target working people on low incomes. “Their ads pop up on computer screens and phones, offering fast access to cash”, according to Cathy O’Neil in her 2016 book Weapons of Math Destruction. A payday loan is a short-term loan with high fees and interest rates that make it a very expensive way to borrow money. You can borrow up to $1,500. You must pay the loan back from your next pay cheque. If you can’t pay it back on time, you face more fees and interest charges that increase your debt. Payday loans are meant to cover a cash shortfall until your next pay.

The Government of Canada has information about pay day loans including the graphic below that starkly shows their high price compared to other forms of borrowing.

Learn your credit score

Credit lets you get goods or services before you pay for them, based on the trust that you’ll pay for them in the future. Credit cards let you buy relatively small things like groceries, and loans, lines of credit and mortgages let you get bigger things like cars or houses.

Your credit report is a summary of your credit history. It’s a record of when you’ve bought things on credit and how well you’ve done at paying things back. How well you’ve done is represented by your credit score, a three-digit number that comes from your credit report. It shows how well you manage credit and how risky it would be for a lender to lend you money.

Why your credit history matters

Financial institutions look at your credit report and credit score to decide if they will lend you money. They also use them to determine how much interest they will charge you to borrow money.

If you have no credit history or a poor credit history, it could be harder for you to get a credit card, loan or mortgage. It could even affect your ability to rent a house or apartment or get hired for a job. If you have good credit history, you may be able to get a lower interest rate on loans. This can save you a lot of money over time. (For more info see Credit report and score basics and Improving your credit score from the Government of Canada.)

Reducing your taxes

Two ways to reduce your taxes are to claim deductions and tax credits on your taxes. Deductions reduce the amount of income you get taxed on, called your taxable income. Tax credits then reduce how much tax you pay on your taxable income.

One of the most common deductions comes from putting money in things like a Registered Retirement Savings Plan (RRSP). You can deduct money you deposit in an RRSP, up to a limit based on, among other things, the income you earned in previous years.

Other deductions include:

- child care expenses for children under 16 years old;

- expenses a person with a disability paid to earn income or go to school; and

- support payments to a spouse, common-law partner or child under a separation agreement or court order. (More info on federal deductions)

Tax credits reduce the tax you pay on your taxable income. The more tax credits that apply to you, the more you can reduce your income tax.

The best known tax credit is the Basic Personal Amount (BPA) which is used to ensure that people making a certain amount, or below, don’t have to pay any federal tax. In 2020, the BPA was $13,229 so anyone making $13,229 or less didn’t have to pay any tax. People earning above this amount were able to claim 15% of $13,229, or $1,984.35. (More info on Tax Credits.)

So increase your financial literacy and share what you learn with others in your community so that everyone can get better at achieving goals like buying a house or paying for their children’s education.

Together we grow stronger – and wealthier.