Ok. I admit that the title of this post isn’t entirely true – but it got your attention didn’t it?

What would seem to be true is that one thing keeping Black folks on the bottom on the Canadian economic ladder is lack of financial literacy. I say “seems” because I couldn’t find any data on financial literacy of Black Canadians. I did find a May 2019 article titled, The State of Financial Literacy in Canada: How Much Do We Know? that cited the 2015 Organisation for Economic Co-operation and Development (OECD) Survey on Measuring Financial Literacy and Financial Inclusion. The survey measured respondents’ financial knowledge, attitudes and behaviours and ranked Canadians’ overall financial literacy third out of 29 countries. The article also cited info from the Canadian Financial Capability Survey showing differences based on gender, age, and education level. However, neither of them mentioned race. So, we must work with anecdotal evidence and assumptions. The first assumption is that a key indicator of the financial literacy of average members of a community is the overall financial health of that community.

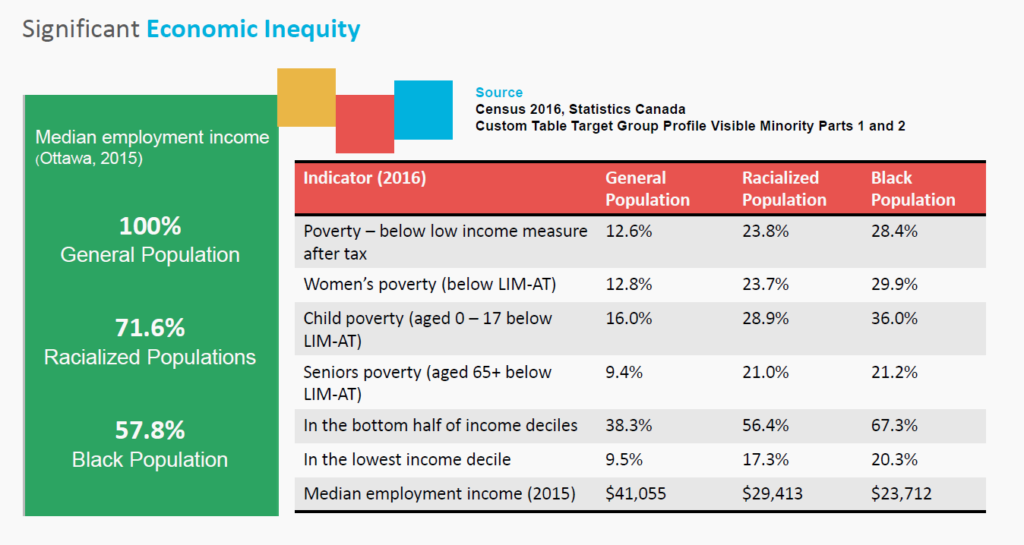

The headline of the August 2020 Summary Portrait of Ottawa’s Black Community in Comparison to the General Population, by the Social Planning Council of Ottawa stated the financial situation of Ottawa’s Black community in starkly clear terms, “The Black community has significantly higher rates of poverty and inequitable employment outcomes in comparison to the general population.” The chart below from the study gives more sobering details.

So, based on the data above, we can assume that many folks in Ottawa’s Black community could use better financial literacy. Yet, during Black history month 2020, I attended many events that were all well attended, except the one on financial literacy. About eight people showed up, about four of whom were members of the presenter’s family. Also, we had a Black Hub Freedom School meeting in September on financial literacy with guest speaker Duane Francis. Duane works with Canada’s only Black billionaire, Michael Lee-Chin, so we thought folks would turn out to hear what he had to say. One person showed up.

In 2003, comedian Dave Chappelle did a sketch called Reparations on his short lived but classic Chappelle Show. The sketch is a satirical news report about Black folks in the US getting their first reparations cheques. It shows Black people gleefully lining up at a liquor store and has a white correspondent reporting from Wall Street on sharp stock price increases for gold, diamonds and fried chicken. The correspondent ends his report with, “Cadillac said they sold 3000 Escalade trucks this afternoon. These people seem to be breaking their necks to give this money back to us.”

Like all good comedy, it’s funny because it reflects some truth. One truth the sketch reflects is that, when Black folks get money, they spend way more of it on short terms gains than they invest for the long term – if they invest any at all.

To be clear, there are many systemic barriers that hamper Black folks from getting money in the first place. But the continuing inter-generational economic challenges of Black communities suggest that, when Black folks overcome those barriers and get some money – they break their necks to give it back.

We need to stop doing this. We need to see financial literacy as essential as basic literacy. No Black parent would not teach their kids to read. So why do so many of us not teach our kids – or ourselves – how to grow wealth over the long term?

It’s time to start financial literacy groups where Black folks regularly meet to increase our financial literacy – together. We need to stop buying lottery tickets with the unrealistic and vague goal of “getting rich” and start setting specific goals, like buying a house, and helping each other create realistic plans to achieve them.

Talking with a financial advisor is good start. They charge for detailed personal advice but many would agree to share general advice with you or your financial literacy group (they might get some paying clients out of it). You can also use online investing tools, or “robo advisors”, like Wealthsimple or CI Direct Investing. I recently signed up with CI Direct Investing that asked me some basic questions about my investing goals and my risk tolerance. It then let me choose a conservative, moderate or aggressive portfolio (only 3 choices which made it easy). The fee is 0.6%, annually, of what you invest. So, if you invest $500, your fee for the year would be $3 – a lot more affordable than most financial advisors.

So what’s stopping you? Set up a group, get online and start learning – and earning.